by

by Financial Pressure on American Households

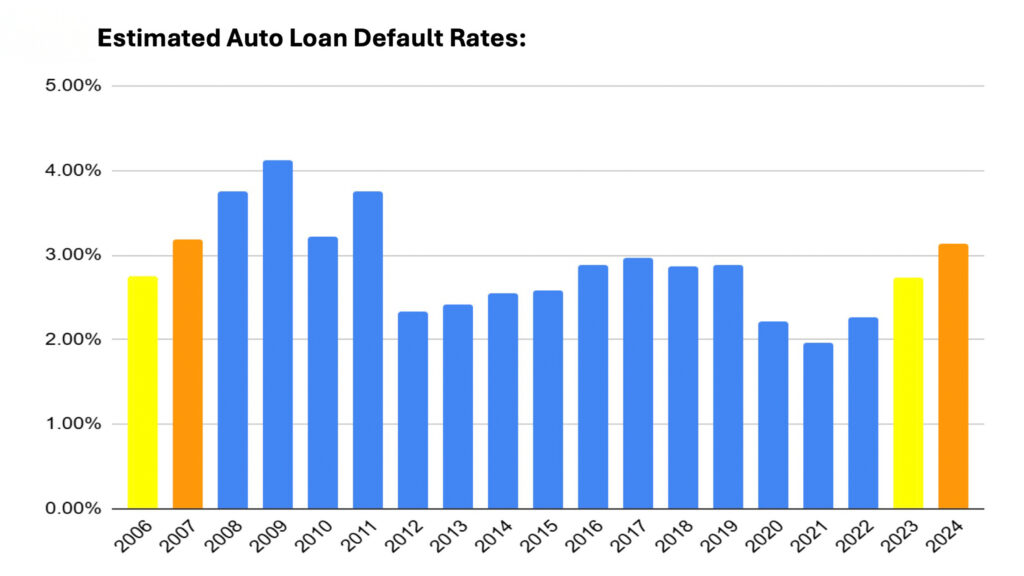

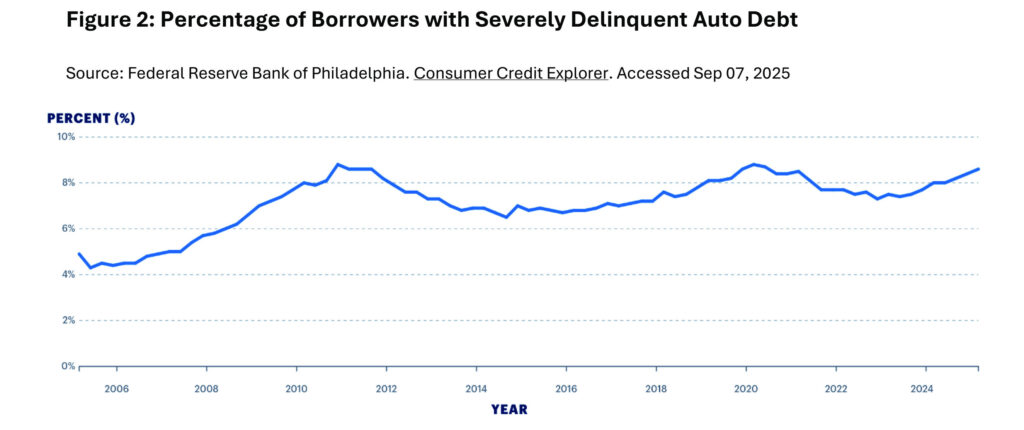

Many Americans adore the feeling of driving a new car, but this pleasure is pushing family budgets to the limit. Auto loan delinquencies are rising, the country owes an incredible $1.66 trillion, and some indicators show frightening parallels with the period just before the 2008 financial crisis.

One in four car trade-ins is now unprofitable, and the situation is worsening

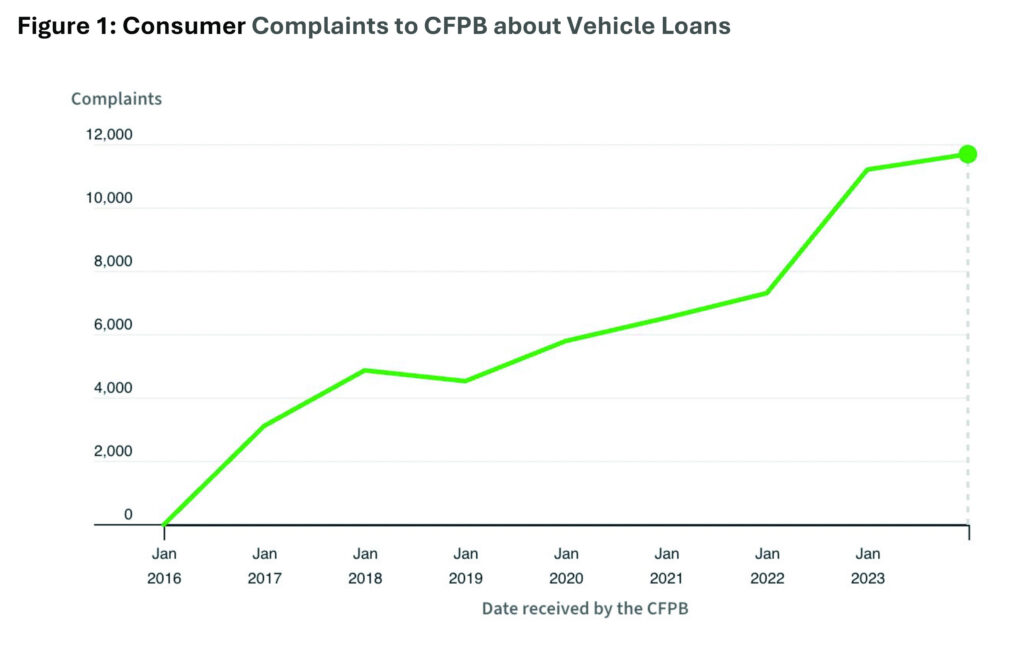

This is reflected in a new report by the Consumer Federation of America titled “Driven to Default: Economic Risks from Rising Auto Loan Delinquencies.” The document describes US auto financing as “on the brink of collapse” and also criticizes Congress and federal oversight bodies for inaction, despite evidence suggesting the need to protect buyers from unscrupulous dealers.

High Monthly Payments

One reason why car owners are on the verge of bankruptcy is the high cost of monthly payments, partly caused by high interest rates. Data shows that the average monthly payment is $745, and 20 percent of buyers have monthly bills of at least $1,000. The situation could quickly worsen, as the $7,500 tax credit for electric vehicles will soon disappear.

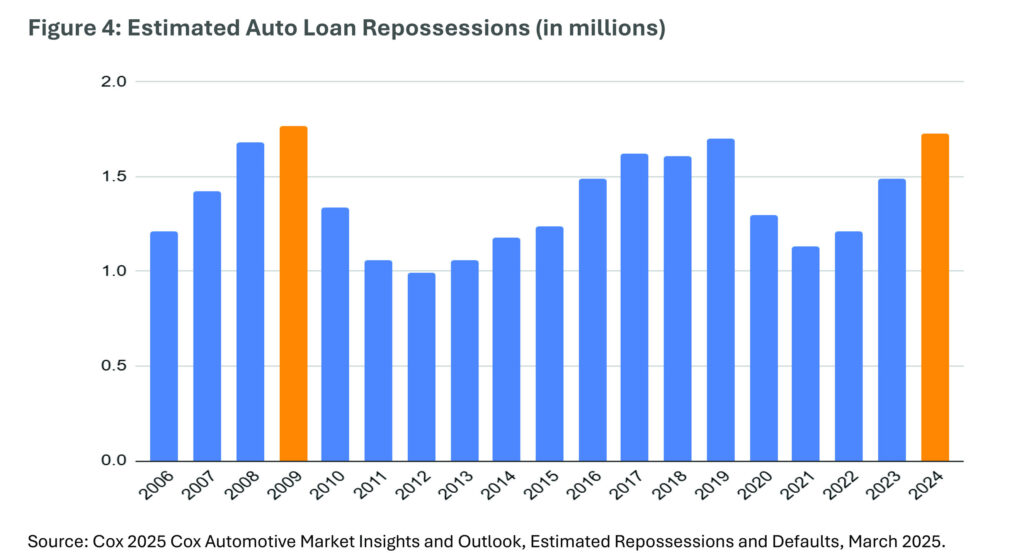

This time, not only subprime borrowers are feeling the pressure. Auto buyers with higher credit scores are twice as likely to be delinquent on payments compared to before the pandemic. Young buyers are massively falling into difficult financial situations, and the rate of repeat car repossessions across all age groups has increased by 43 percent between 2022 and 2024, according to Cox data.

A Warning for the Entire Economy

Furthermore, the CFA warns that we should be concerned not only about car repossessions due to non-payment. Americans tend to prioritize car payments over other expenses, meaning that delinquency levels may indicate much broader and more serious problems in the US economy.

Now is the time for policymakers to carefully examine the auto lending market to expose exploitative practices that drive up prices and demand that federal regulators wake up from slumber during this crisis while Americans suffer

Personal Decisions and Societal Consequences

However, the question remains: do drivers really need intervention from legislators, or is part of the solution to make different choices? The obvious way to avoid this situation is to be honest with yourself about your financial status and buy a well-maintained used car. I broke the habit of leasing cars five years ago and haven’t regretted it since. But everyone does what they like, right?

This auto loan situation could have far-reaching consequences, as a car is often not just a means of transportation but a necessity for work and daily life. The rise in delinquencies may point to deeper structural problems, such as income inequality or insufficient household savings, making them vulnerable to any economic shocks.