by

by Electric vehicles are becoming a serious headache for the insurance industry. The latest report from Mitchell, a developer of software for managing post-accident recovery, shows a sharp increase in the number of insurance claims related to EV repairs.

Rise in Claims Against a Backdrop of Falling Sales

These figures look especially impressive against the backdrop of slowing electric vehicle sales growth in 2025. This happened due to the expiration of government tax incentives and a shift in consumer interest towards hybrids. According to Cox Automotive estimates, sales of new EVs in the US fell by approximately 2%. Even Tesla’s market share slightly decreased, dropping to 46.2% from 48.7% in 2024, as competitors strengthened their positions.

Repair Complexity as a Key Problem

The existing fleet of electric vehicles is aging and getting into more accidents, and the complexity of their repair is becoming a logistical and financial obstacle for the recovery industry.

Ryan Mandell, Vice President of Strategy and Market Intelligence at Mitchell, explained: “Due to their dense electrical architecture, software-controlled systems, and interconnected designs with a large number of sensors, these vehicles require additional diagnostic and calibration operations when damaged. This can increase the cost, complexity, and cycle time of each repair.”

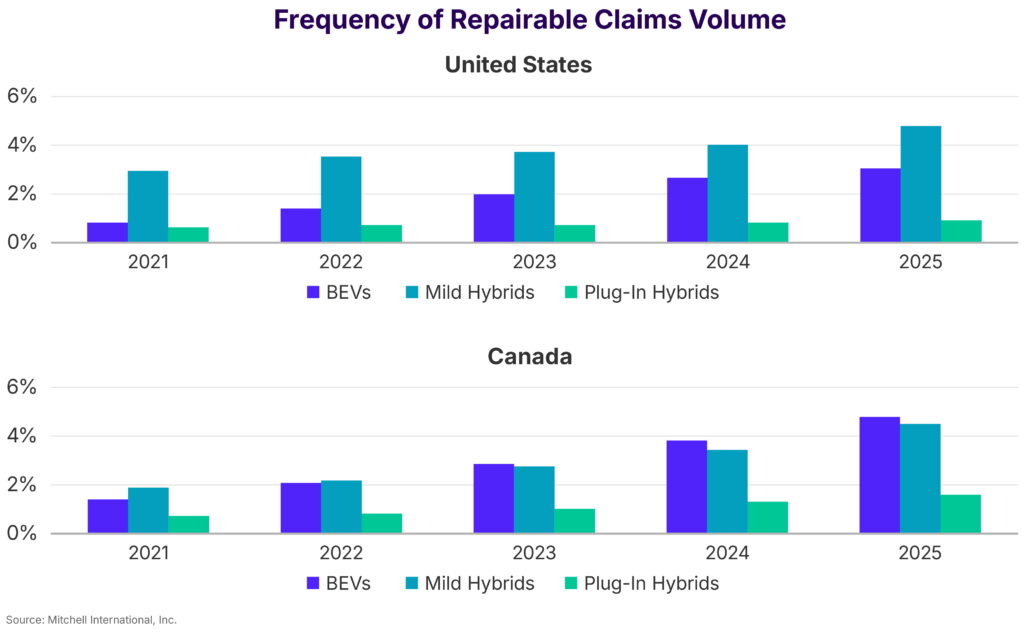

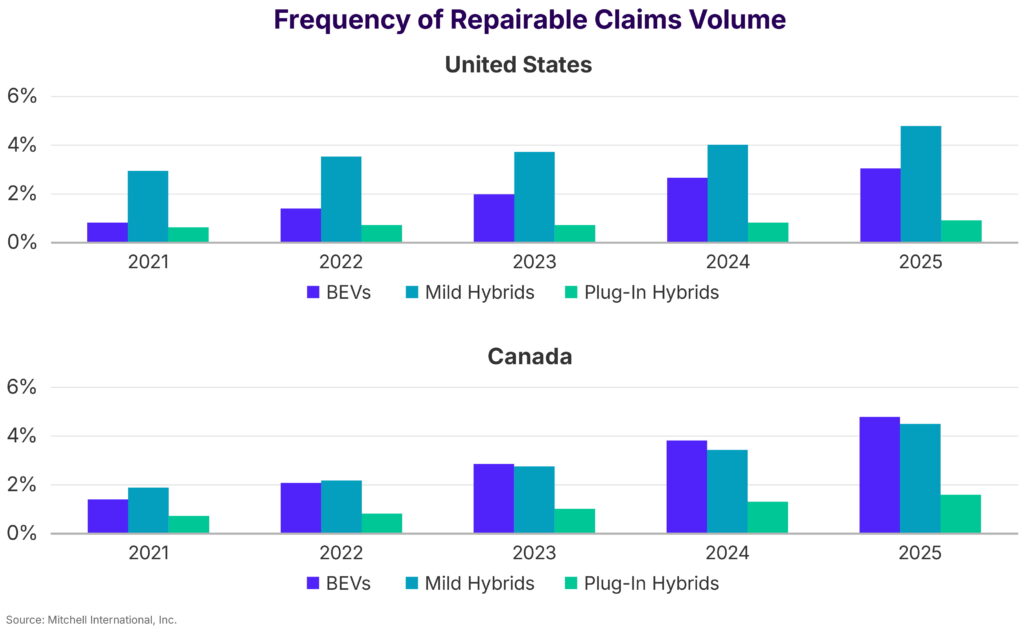

The “Plugged-In: EV Collision Insights” report also examined other types of electric vehicles. The number of repairable claims for plug-in hybrids (PHEV) increased by 6% in the US and by 26% in Canada in 2025. For mild hybrids (MHEV), the growth rates were 20% in the US and 29% in Canada. It is worth noting that MHEV sales in the US surged by 28% in 2025.

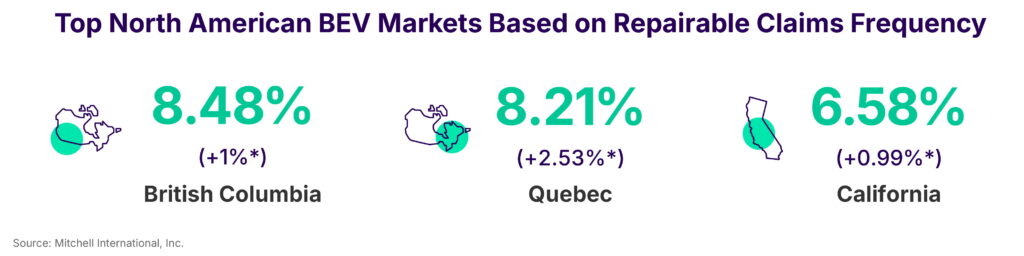

In North America, the highest demand for EV repair was recorded in British Columbia (8.48%), followed by Quebec (8.21%) and California (6.58%).

Which Models Lead in the Number of Insurance Claims?

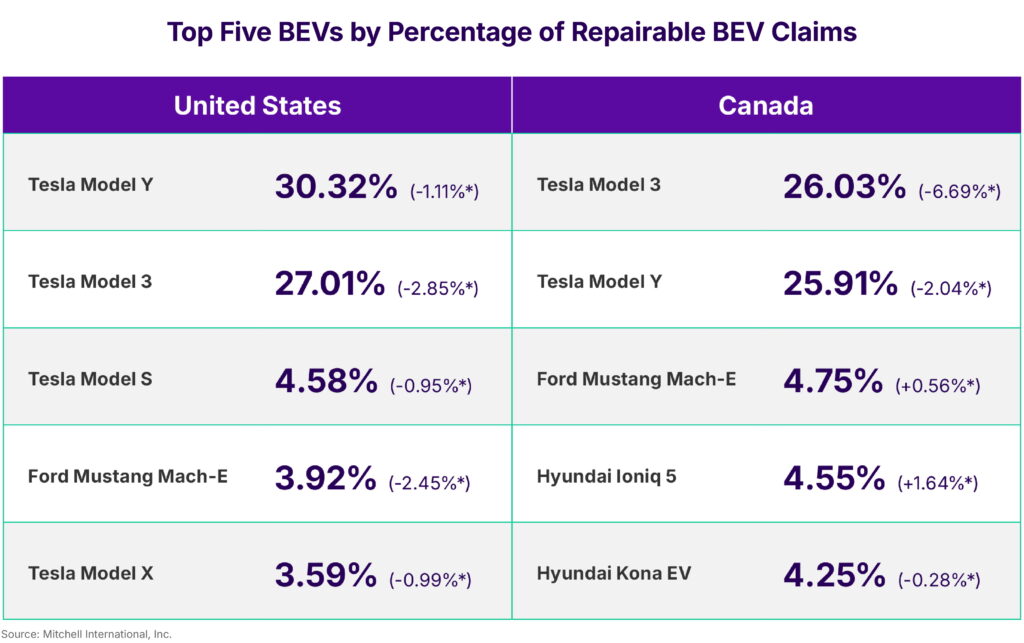

Looking at individual models, Tesla continues to dominate in claim volume. In the US, the Model Y accounts for 30.32% of repairable claims for battery electric vehicles (BEV), followed by the Model 3 with 27.01%. Together, these two models account for more than half of all such claims. In Canada, the picture is similar, although the positions are reversed: the Model 3 with 26.03% slightly edges out the Model Y with 25.91%.

The Economics of Electric Vehicle Repair

There is also good news. In terms of repair, the average cost of restoring an EV fell by 5% in the US – from $6,707 to $6,395, and decreased by 2% in Canada in 2025. For ICE vehicles and PHEVs, prices in the US remained almost unchanged, while for MHEVs the average claim cost increased by 4% – from $4,865 to $5,054.

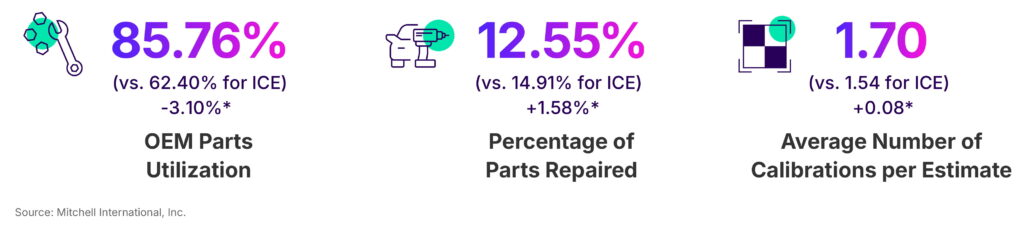

However, the greater complexity of electric vehicle repair is reflected in their “calibrations per estimate” rating, which tracks how often sensors and systems need to be recalibrated after repair. In 2025, the average number of such operations was 1.70 for EVs and 1.63 for hybrids, compared to 1.54 for ICE vehicles.

Mitchell’s data also shows that 86% of parts costs for EVs are for original equipment manufacturer (OEM) components, with only 13% of parts considered repairable rather than replaceable. For ICE vehicles, 62% of parts costs go to OEM components, and 15% of parts are considered repairable.

The Depreciation Trap

Mitchell also reported that the market value of total loss vehicles decreased in 2025 for most powertrain types, with EVs showing the sharpest decline. In the US, EV value fell by 6% – from $30,126 in 2024 to $28,185 in 2025. In Canada, they fell by 13% – from $41,775 to $36,504 Canadian dollars.

For comparison, the value of ICE vehicles decreased by 2.55% in the US and by 6.12% in Canada. Hybrids presented a more mixed picture: in the US their value increased by 4.18%, while in Canada it fell by 4.40%.

These trends indicate a complex transitional period for the electric vehicle market. On the one hand, direct repair costs are beginning to decrease slightly, possibly due to workshops accumulating experience and the development of the parts market. On the other hand, structural factors such as high dependence on original parts and the complexity of calibrations continue to make each incident expensive and time-consuming. The sharp depreciation is likely a consequence of the rapid technological obsolescence of early models, the emergence of new, more affordable options, and some market consolidation. For owners, this means that, despite somewhat smaller repair bills, the total cost of ownership due to loss of market value can be significant. For the insurance industry, developing models that adequately account for these opposing trends – somewhat lower operational repair costs, but significantly greater total loss risks – remains a key challenge.