by

by If you feel like your auto loan is dragging you under, you are not alone. New data from Edmunds shows that American car buyers are sinking deeper into a financial “underwater current” than ever before, and the situation is worsening every month.

Record Negative Equity Figures

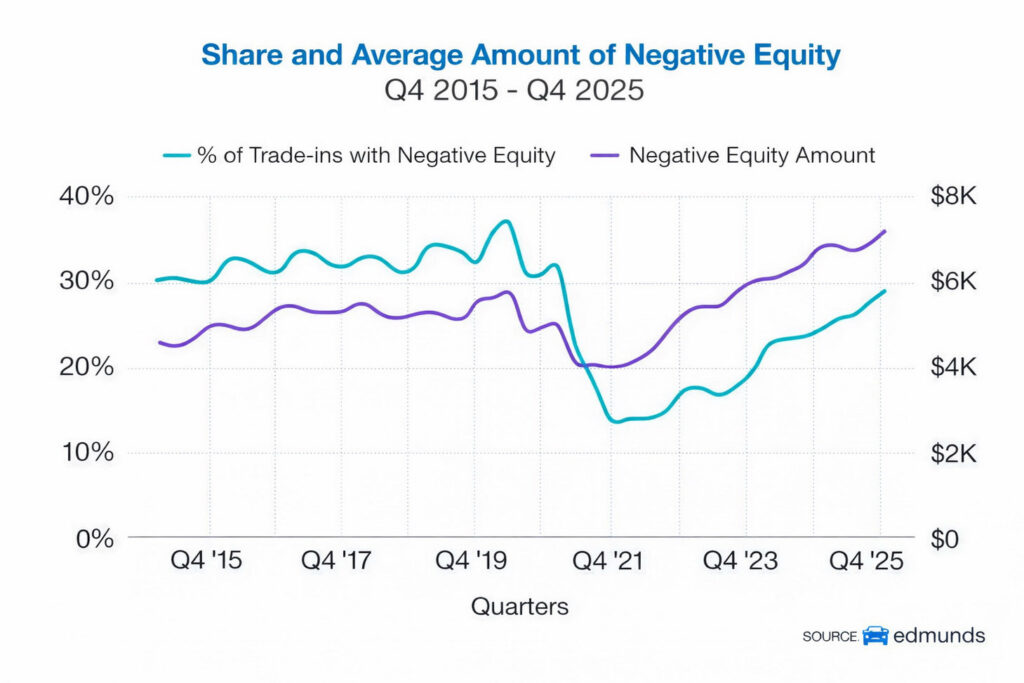

In the last quarter of 2025, a full 29.3% of people who traded in their car when buying a new one owed the bank more than their car was worth. This is the highest figure since the first quarter of 2021.

Even worse, the average amount of negative equity reached a record $7,214. A growing share of buyers are finding themselves not just slightly “negative,” but dramatically underwater.

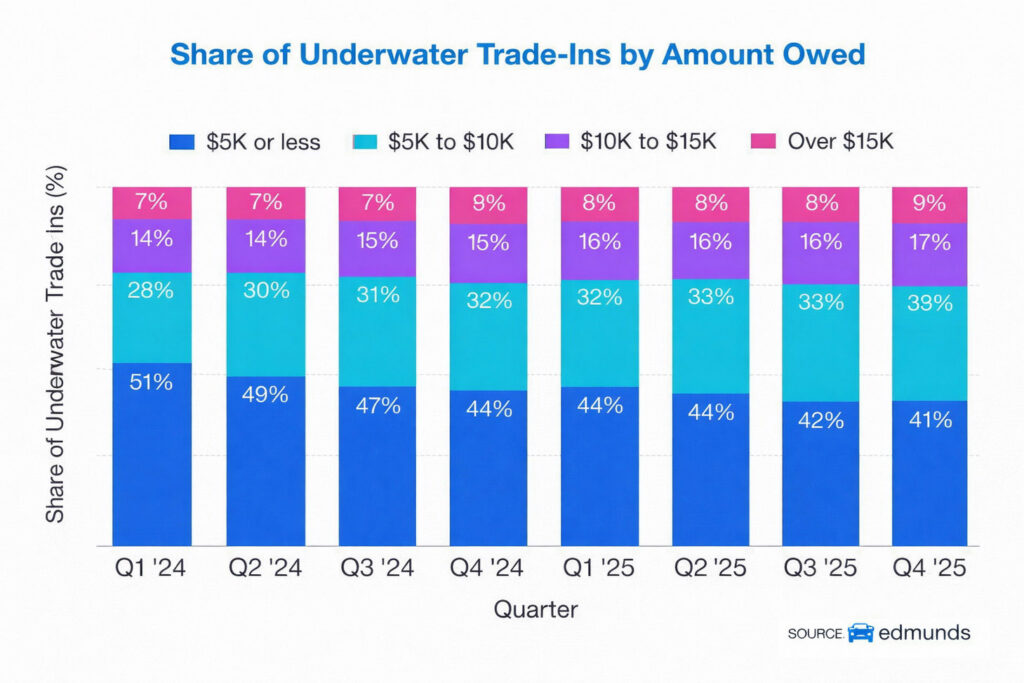

Over a quarter of such “underwater” trade-ins had a debt of at least $10,000, which is also a historical maximum. Specifically, 27% of such deals in the fourth quarter of 2025 had a five-figure “negative” balance: 17.4% owed between $10,000 and $15,000, and 9.2% owed over $15,000.

Almost one in ten drivers arrived at the dealership buried under over $15,000 of debt even before choosing a new car. This is no longer just financial inequality on the road, but a real abyss.

Reasons for the Growing Problem

The problem has been brewing for years. Many of these loans were taken out during the pandemic and chip crisis when cars were scarce and prices were sky-high. Buyers paid close to or even above the sticker price and often stretched loan terms to make payments affordable. Now those same cars are worth less, while the loan balances remain stubbornly high.

When drivers change cars early, they typically “roll over” this residual debt into the next loan. According to Edmunds, buyers with negative equity financed an average of $11,453 more than regular buyers. Their typical monthly payment rose to $916, significantly higher than the industry average of $772.

To make these payments feel smaller, more and more people are choosing 84-month loans, which only prolongs the problem over time. Longer loans mean slower reduction of the principal, making it more likely that the next trade-in will also be “underwater.” Edmunds reports that nearly 41% of new car purchases with negative equity are financed with 84-month loans.

The Price of Replacing a Car Too Early

This becomes a financial merry-go-round that never stops spinning. Experts say the best rescue plan is simple but not always easy: keep the car longer if possible, make extra payments to reduce the principal, and avoid “rolling over” debt into the next purchase.

If you really want to sell, try doing it privately rather than through a trade-in. This might help you get more money to cover the loan, — noted Bruce McClary, senior vice president of the National Foundation for Credit Counseling.

This situation points to a deeper systemic problem of car affordability and financial literacy. Record amounts of negative equity are not only a personal problem for owners but also a potential risk to the credit system as a whole if economic conditions worsen. The trend towards extremely long loans is creating a generation of drivers who may never fully own their car, constantly refinancing old debt. Escaping this cycle requires both personal discipline in financial planning and, perhaps, a review of market practices regarding the promotion of excessively long loan terms.