According to recent data, interesting shifts are occurring in the US electric vehicle market. The traditional leader, California, is showing signs of market fatigue, while other states, on the contrary, are demonstrating rapid growth.

Decline in California

After many years of leading the national transition to electric vehicles, California may be approaching a tipping point. For the first time since the pandemic, EV sales in the state are expected to fall in 2025, even as several other states report a sharp increase in their popularity.

California Has a New Way to Make EV Owners Pay

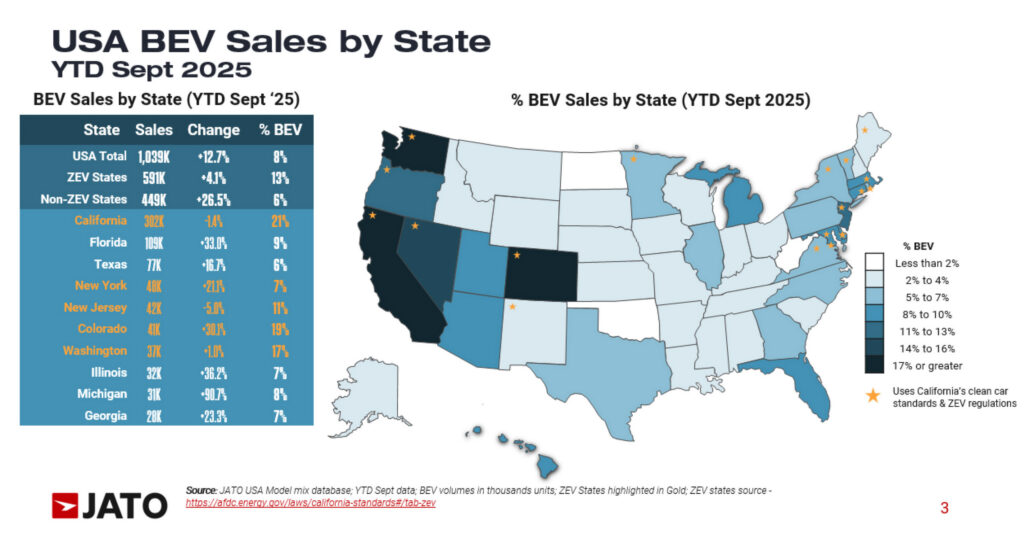

Data from JATO Dynamics shows that during the first nine months of 2025, before the federal EV tax credit expired, approximately 302 thousand electric vehicles were sold in California. This figure represents a decrease of 1.4 percent compared to the same period last year, hinting at a possible saturation of the state’s market.

Final figures for the last quarter of the year are not yet available, but given the cancellation of the $7,500 federal tax credit on September 30, it is safe to assume that the final numbers will be worse unless buyers suddenly developed a taste for higher costs.

Leadership Remains, But Competitors Are Catching Up

Despite this, California remains significantly ahead of everyone else. Electric vehicles now account for 21 percent of new car sales in the state, placing it above the District of Columbia (19 percent), Colorado (19 percent), Washington (17 percent), Nevada (16 percent), and Oregon (13 percent).

Rapid Growth in ZEV Program States

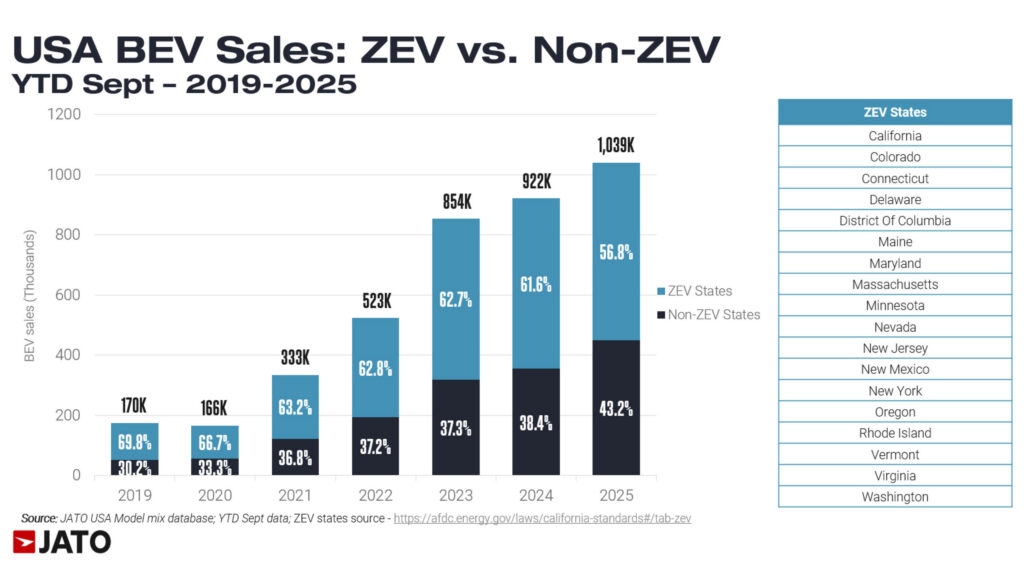

Several of these states that adhere to the Zero-Emission Vehicle (ZEV) program showed noticeable progress last year. For example, electric vehicle sales in New York increased by 21.1 percent in the first three quarters, while Colorado showed an increase of 30.1 percent. On average, electric vehicles account for 13 percent of new car sales in ZEV states. In contrast, in states not part of the program, the average is only 6 percent, forming a national average of 8 percent.

Unexpected Growth Leaders

Electric vehicle sales also surged sharply in many non-ZEV program states during the same period. Florida, in particular, recorded an impressive jump of 33 percent between January and September 2025, reaching 109 thousand units, which now accounts for 9 percent of new car sales.

This jump in Florida is notable not only for its scale but also because it occurred without the support of ZEV mandates or aggressive state-level incentives. In a politically conservative state where environmental policy is not a priority, this growth indicates that consumer demand, not legislation, is doing the main work.

Texas followed Florida with growth of 16.7 percent to 77 thousand units. Illinois demonstrated an increase of 36.2 percent, reaching 32 thousand. Georgia showed growth of 23.3 percent to 28 thousand, while Michigan led in growth rate, increasing sales by 90.7 percent to 31 thousand electric vehicles sold.

The rapid growth of electric vehicle sales in Michigan is a prime example of why growth in traditionally non-ZEV states represents such a valuable opportunity for domestic brands. While a brand can break into a new market, as Tesla did nationally, we expect electric vehicle sales in other states to come from brands that the population is already familiar with.

The Charging Infrastructure Problem

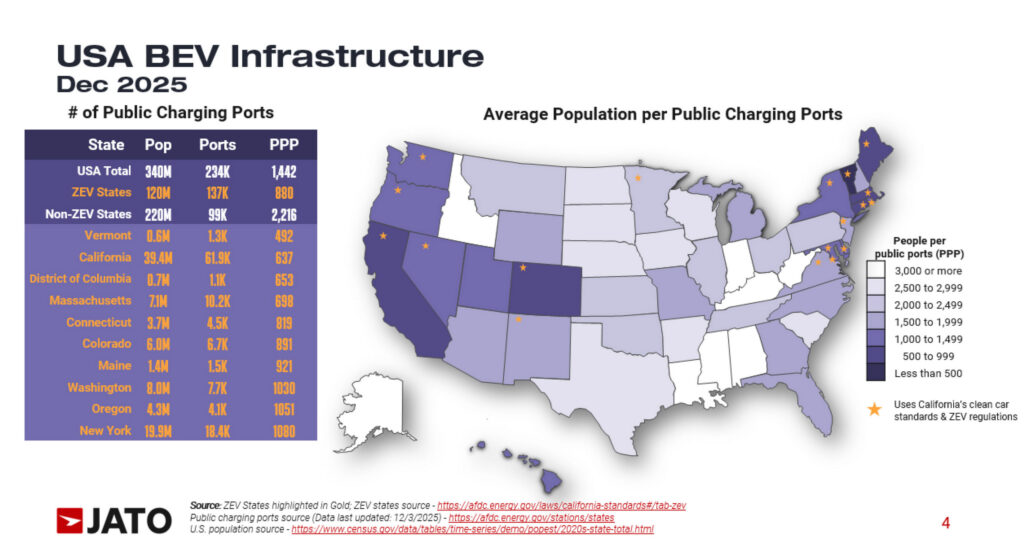

One of the key obstacles to the spread of electric vehicles in non-ZEV program states remains charging infrastructure. In ZEV states, there is approximately one public charging point per 880 people. In non-program states, this figure increases significantly – one point per 2,216 people, indicating a critical gap in support systems for electric vehicle owners.

This data suggests that the US electric vehicle market is entering a new, more mature phase, where the initial leadership of individual regions is gradually leveling out. Growth in states like Florida or Michigan shows that the technology is beginning to overcome political and regional barriers, becoming more mainstream. However, as experts note, further success will depend not only on the supply of vehicles but also on the ability of infrastructure, especially the charging station network, to catch up with consumer needs in all corners of the country. This creates both challenges and enormous opportunities for automakers, especially those with strong positions in the domestic market.