by

by Americans are increasingly taking out auto loans for over six years

Americans are borrowing more and more money and stretching out repayment terms to buy a new car. This is leading to an increase in the number of buyers who pay over $1,000 per month. This situation is a serious reminder of how easily one can fall into debt trying to pay off an auto loan.

A new analysis by Experian Automotive shows that the share of new cars bought on credit for a term of over six years rose to 35.6% in the first quarter, compared to 30.8% a year earlier. Even more striking is that 3.3% of new car buyers are now signing loans for 85 months or more, up from 2.9% last year.

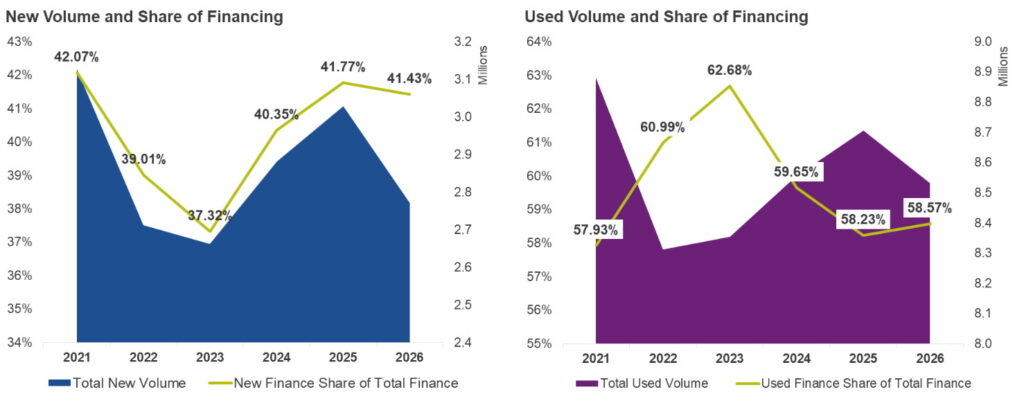

The situation in the used car market

The same trend is seen in the used car market: the share of loans for terms over six years rose from 28.6% to 31.5%, and those exceeding 85 months — from 1.3% to 1.4%. Melinda Zabritski of Experian noted that affordability remains a key factor in financial decisions, and more consumers are choosing long-term loans to make monthly payments manageable.

Increase in average payments

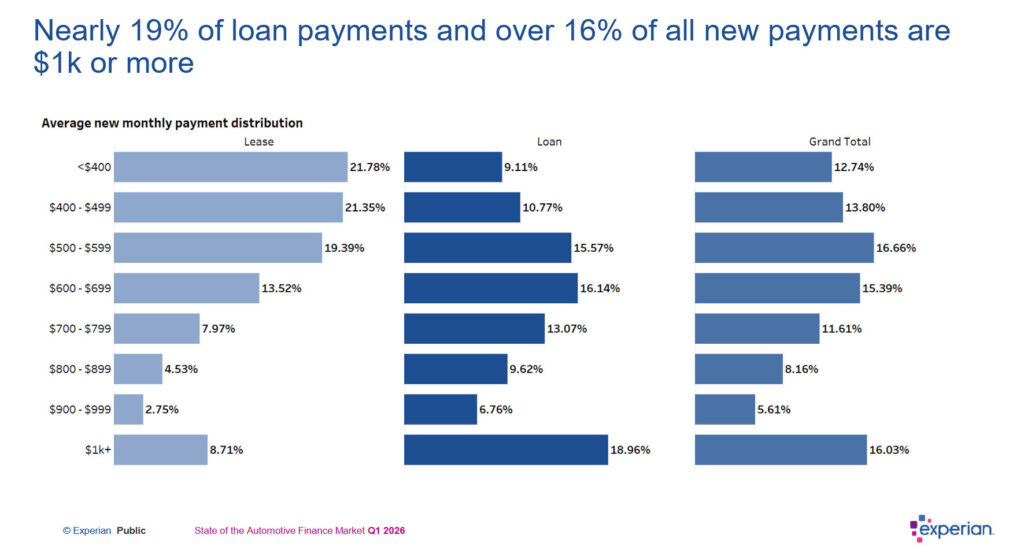

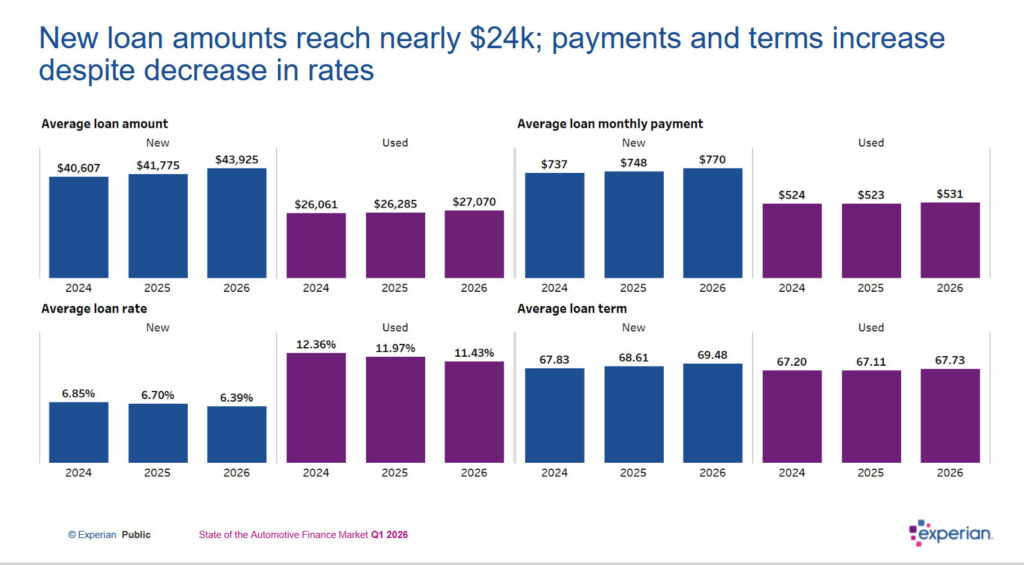

The numbers are telling. In the first quarter of 2026, the average loan for a new car rose by $2,150 compared to last year, reaching $43,925. This pushed the typical monthly payment from $748 to $770. As expected, more buyers are now paying over $1,000 per month. However, not everyone is in this situation: nearly 20% of new loans still have monthly payments below $500.

Debt burden is growing

An analysis of over 5 million open auto loans and leasing agreements shows that nearly 19% of them for new cars exceed $1,000 per month, up from about 17.4% at the same time last year. This is not related to buyers choosing more expensive models. In fact, among loans with monthly payments over $1,000, about 74% are for non-luxury models, often including expensive pickup trucks such as the Chevrolet Silverado 1500, Ram 1500, and Ford F-150.

According to CNBC, just five years ago, only 5.4% of new car loans had monthly payments exceeding $1,000. However, since prices for new cars skyrocketed after the Covid-19 pandemic and the semiconductor shortage, loan payments have also increased.

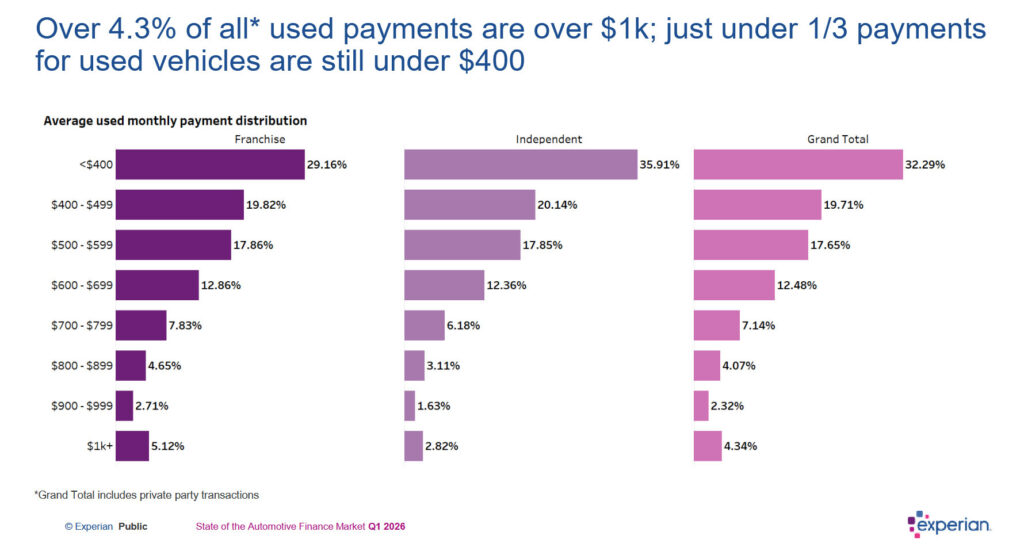

This applies not only to new cars. The average loan amount for a used car also rose by $785 compared to last year, reaching $27,070 in the first quarter. Additionally, the average monthly payment increased from $523 to $531.

Experian also found that the average loan term for a new car reached 69.5 months, while loans for used cars averaged 67.7 months. Separately, consumers who refinanced their auto loans lowered their interest rates by an average of 2.2 percentage points and reduced their monthly payments by $81.

These figures indicate that the financial pressure on American drivers continues to grow. Longer loan terms, while making monthly payments more affordable, lead to a significant increase in the total amount of interest paid. This could create a risk for household financial stability, especially in an environment of economic uncertainty. Furthermore, the fact that most large monthly payments are for non-luxury models, particularly pickup trucks, suggests that even basic vehicles are becoming increasingly expensive, forcing buyers to take on greater financial obligations.